Why Global Diversification Still Matters

If you look at market headlines over the last decade, it feels like one story. US large-cap stocks, especially big tech, the Magnificent 7, and the S&P 500, have outperformed.

Many investors have responded by concentrating their portfolios in the S&P 500. Some have gone even further and overweighted the technology sector, often into individual technology stocks that are also overweight in the S&P 500.

One can understand why investors have concentrated on large-cap US equity. The returns have been strong. The companies are innovative. The headlines reinforce the narrative.

But have we gone too far? Should we be considering international equity? Here is the case for why global diversification still matters.

The “Lost Decade”: A Reminder

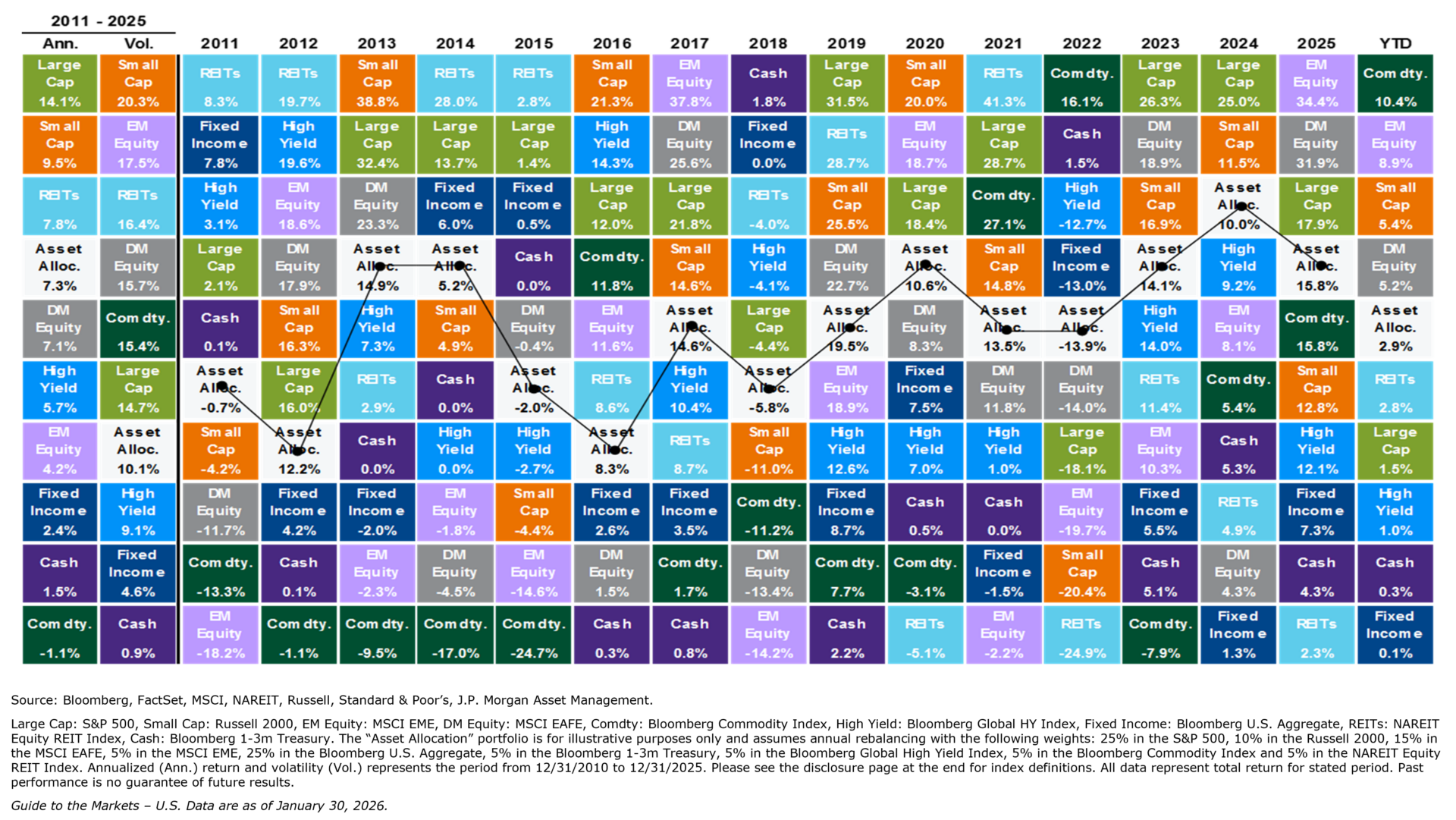

From 2000 through 2009, the S&P 500 delivered a negative annualized return. It was one of the worst ten year stretches in modern US market history.

An investor who owned only the S&P 500 during that period experienced a lost decade.

However, a globally diversified portfolio that included international developed markets, emerging markets, and smaller US companies produced positive returns over that same stretch.

Why?

Because while US large-cap stocks struggled after the dot com bubble burst and during the financial crisis, other areas of the market performed better. Emerging markets had strong years. International stocks outperformed. Small caps had periods of relative strength.

The key lesson is not that international always wins. It does not. The lesson is that markets are unpredictable and global diversification helps protect against downside risk.

When one region or asset class struggles, another can offset it.

Staying Invested in the US – Concentration Risk

None of this means you should abandon US stocks.

The United States remains home to many of the world’s most innovative and profitable companies. Over long periods, US equities have delivered strong returns and have been an important driver of global growth.

Large-cap US stocks deserve a meaningful place in a globally diversified portfolio.

The issue I see today is not underexposure. It is concentration.

Many portfolios are effectively S&P 500 portfolios. Some are even more concentrated in technology because the S&P 500 itself is heavily weighted toward a small group of mega cap companies.

At times, the technology sector and top 10 companies have represented an unusually large share of the index. That means investors may believe they are diversified because they own 500 companies, but in reality, a large portion of their return is coming from a handful of stocks.

That is not necessarily bad. It is simply a risk that should be acknowledged.

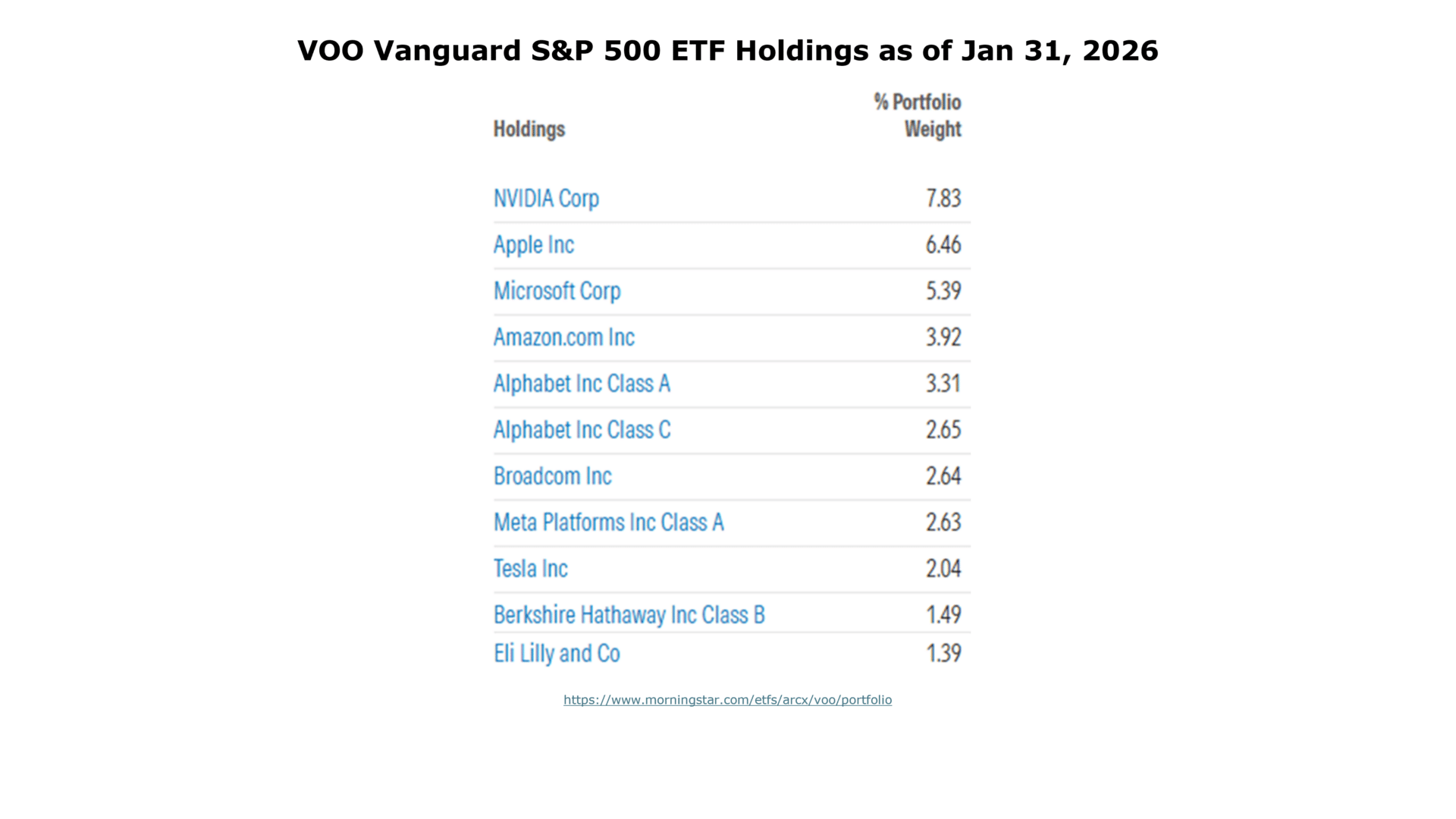

Key takeaways from observing the Vanguard S&P 500 ETF as of January 31, 2026:

- The Magnificent 7 represents approximately 34.23% of the total market capitalization.

- The technology sector represents approximately 34.13% of the total market capitalization. When you include technology adjacent companies that are classified in other sectors, the effective exposure to growth oriented mega-cap companies is even higher.

- The top 10 companies represent approximately 39.75% of the total market capitalization.

Valuations and Global Opportunity

Another reason to consider international equity is valuation.

At various points in history, international markets have traded at lower forward price to earnings ratios compared to the US. When one market trades at a meaningful premium to another, future returns often revert toward more normal levels over time.

Valuation is not a timing tool. Expensive markets can stay expensive. Cheap markets can stay cheap.

But long-term expected returns are influenced by starting valuations. When international markets trade at a discount relative to the US, that can improve their long-term return potential.

Owning both US and international equity allows you to participate wherever growth and reversion occur.

The Small-Cap and Value Premiums

Diversification is not only about geography. It is also about size and style.

Historically, smaller companies have delivered higher average annual returns than large companies. This is often referred to as the small-cap premium.

Similarly, value stocks, those trading at lower valuations relative to fundamentals, have historically outperformed growth stocks over very long-term horizons. This is known as the value premium.

These premiums do not show up every year. In fact, there have been extended periods when large-cap growth stocks dominated.

Does this sound familiar?

Long-term data across decades and across countries suggests that exposure to small-cap and value factors has been rewarded over time.

If a portfolio is concentrated only in US large-cap growth stocks, it misses those additional sources of expected return.

A globally diversified portfolio that includes US small-cap and US mid-cap, as well as international developed and emerging markets equity broadens the opportunity set.

Currency and Cycles

International returns are also influenced by currency movements.

There have been multi-year periods when a declining US dollar boosted returns for US investors owning foreign stocks. There have also been periods when a strong dollar weighed on those returns.

These currency cycles often align with relative economic cycles. When the US dollar weakens, international markets have historically had stretches of outperformance.

Again, this is not a prediction. It is a reminder that global market cycles rotate.

Owning international equity provides exposure to those cycles instead of betting entirely on one economy and one currency.

Global Diversification: Key Takeaways

- Stay invested in the United States equity markets.

- US large-cap equity is an important core holding.

- Recognize the concentration risk that comes from overweighting the S&P 500 and big tech.

- Remember the “Lost Decade” from 2000 to 2009. Investment markets can go through long stretches of disappointment.

- Understand that small cap and value premiums have existed historically, even though they can disappear for years at a time.

- Acknowledge that international markets trade at different valuations, operate under different economic cycles, and can provide diversification benefits when US stocks struggle.

Global diversification is rarely exciting in the short term. It often feels unnecessary when one area is dominating. But over decades, global diversification allows investors to stay disciplined and on track with their financial plan without going all in on a single country, sector, or narrative.

In my experience, the goal is not to guess and try to win the current year. The goal is to build a globally diversified portfolio based on your unique situation that helps you stay on track toward your financial goals.

Global diversification, including US and international stocks across large-cap, mid-cap, and small-cap, as well as US and international bonds, remains one of the most practical ways to pursue that outcome.

While this discussion has focused primarily on equities, similar principles apply to fixed income. Interest rate cycles, inflation trends, and currency movements vary globally as well.

Interested in working together?

Learn more about our complimentary 4-step process sharing how to minimize taxes, invest smarter, and make work optional. This process is designed to help decide if working together makes sense.

More Resources

2026 Market Outlook Planning Takeaways

2026 Important Planning Numbers? (Free PDF resource)

Financial Planning for Dell Employees

Financial Planning for Tech Professionals

Financial Planning for Approaching Retirement

* Historical returns and historical inflation figures are based on long-term data from sources such as S&P Dow Jones Indices LLC, Dimensional Fund Advisors, and JPMorgan, typically covering multi-decade periods and rounded for planning purposes.

Risk Disclosure: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific situation with a qualified tax professional.

Disclosure: Safe Landing Financial LLC is a registered investment adviser. This communication is not intended as an offer or solicitation to buy, hold or sell any financial instrument or investment advisory services. Safe Landing Financial does not guarantee the accuracy or the completeness of any description of securities, markets or developments mentioned. Please visit our website for important disclosures.

Safe Landing Financial Newsletter

Sign up for monthly planning insights for tech professionals and pre-retirees!