Amazon Mega-Backdoor Roth: Tax-Efficient Retirement Savings in 2025

Learn how Amazon’s mega-backdoor Roth strategy helps employees boost retirement savings beyond standard limits and enjoy tax-free growth. This powerful strategy allows after-tax contributions to grow tax-free, offering a significant advantage for long-term wealth accumulation.

In this guide, you’ll learn everything about Amazon’s mega-backdoor Roth, including how it works, contribution limits, tax implications, and case studies to help you decide if it’s right for you.

How Amazon’s Mega-Backdoor Roth Works

The mega-backdoor Roth is a strategy for saving more aggressively and tax-efficiently for retirement by making after-tax contributions to a 401(k) plan and then converting those contributions to a Roth IRA or Roth 401(k).

To avoid a future tax headache, it is critical for Amazon employees to convert after-tax 401(k) contributions to either a Roth 401(k) or Roth IRA.

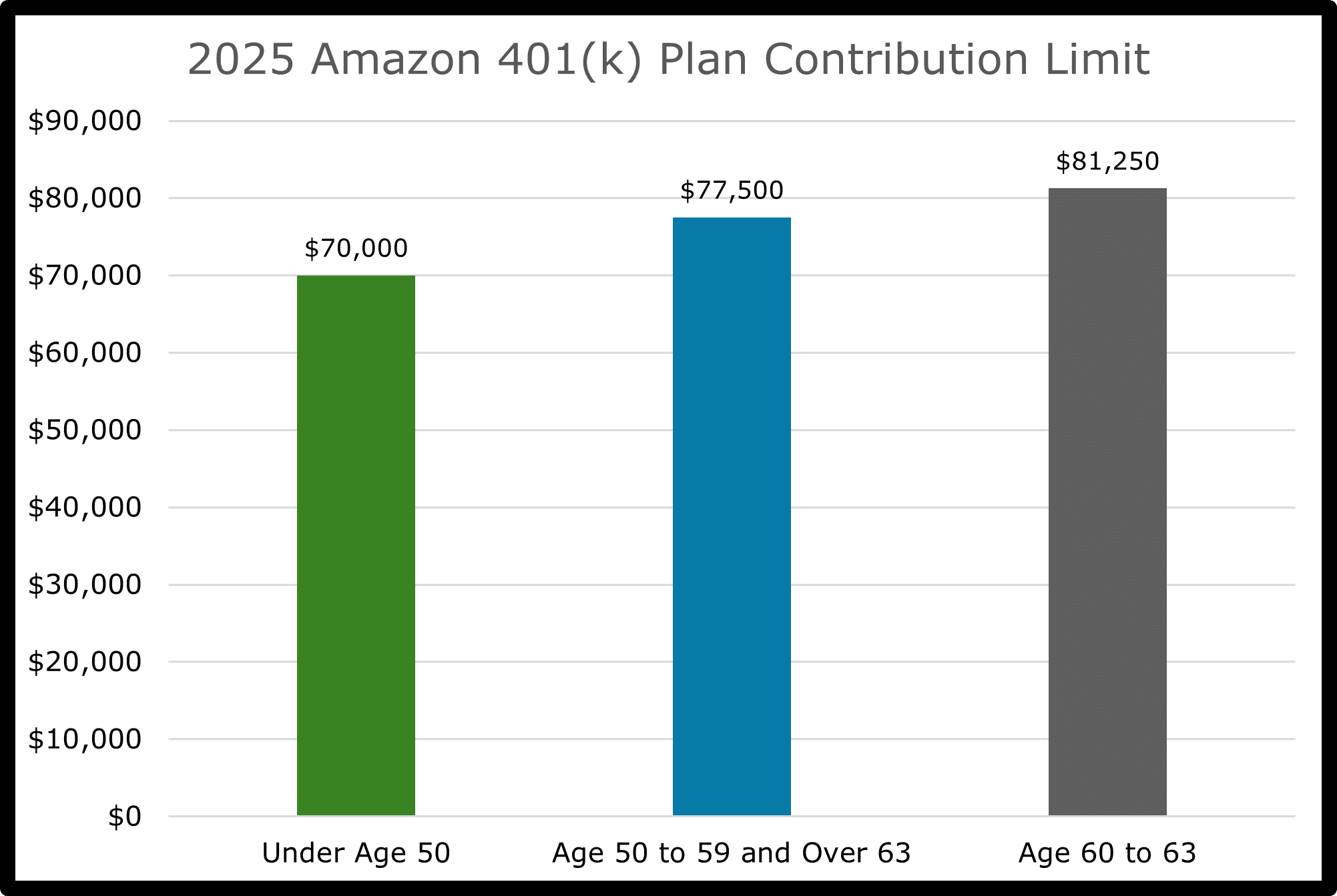

2025 Amazon 401(k) Total Contribution Limits by Age

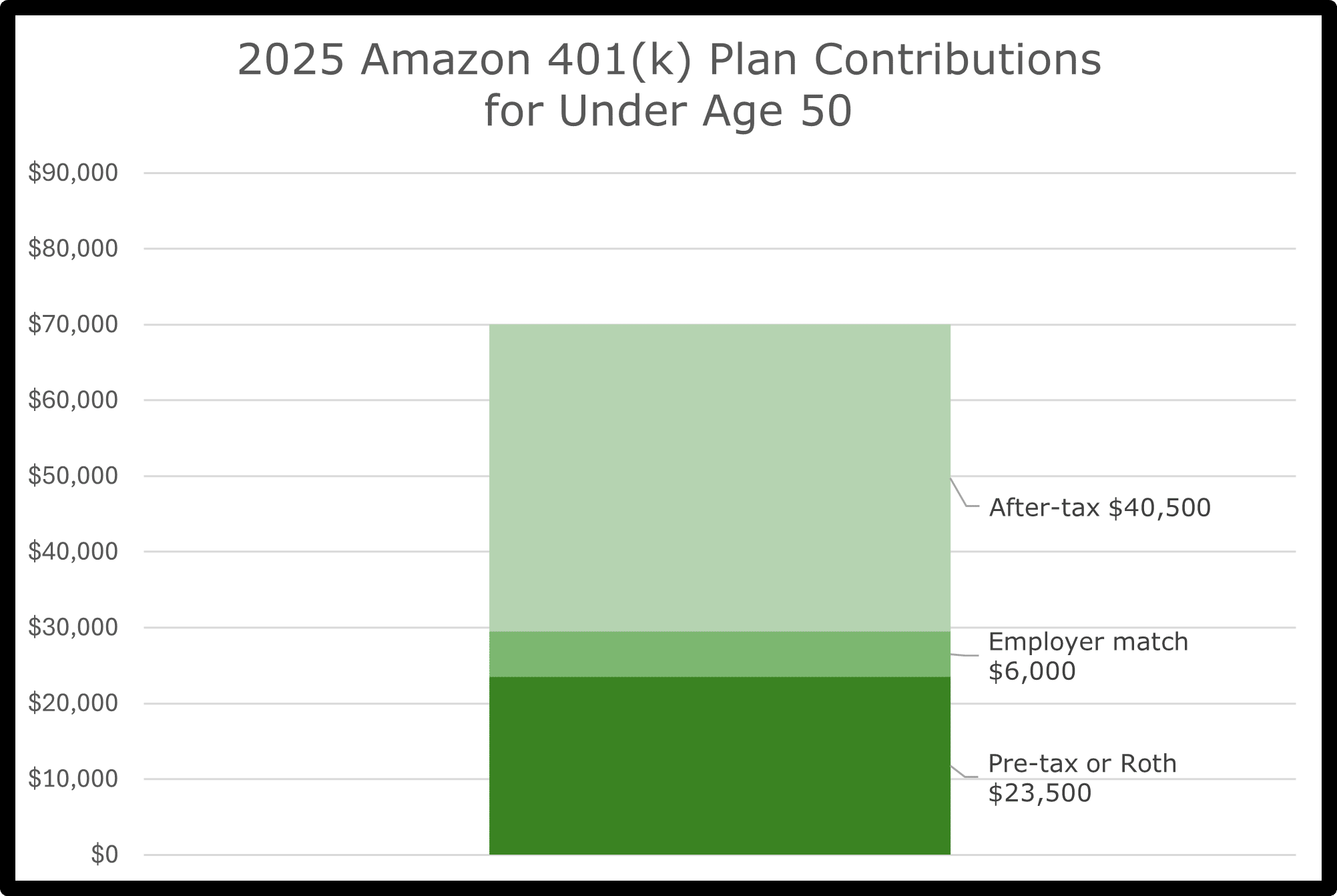

Under Age 50

- Elective deferral: $23,500

- Employer match: Up to $7,000*

- Catch-up contribution: None

- After-tax contribution: ~$40,000**

- Total limit: $70,000

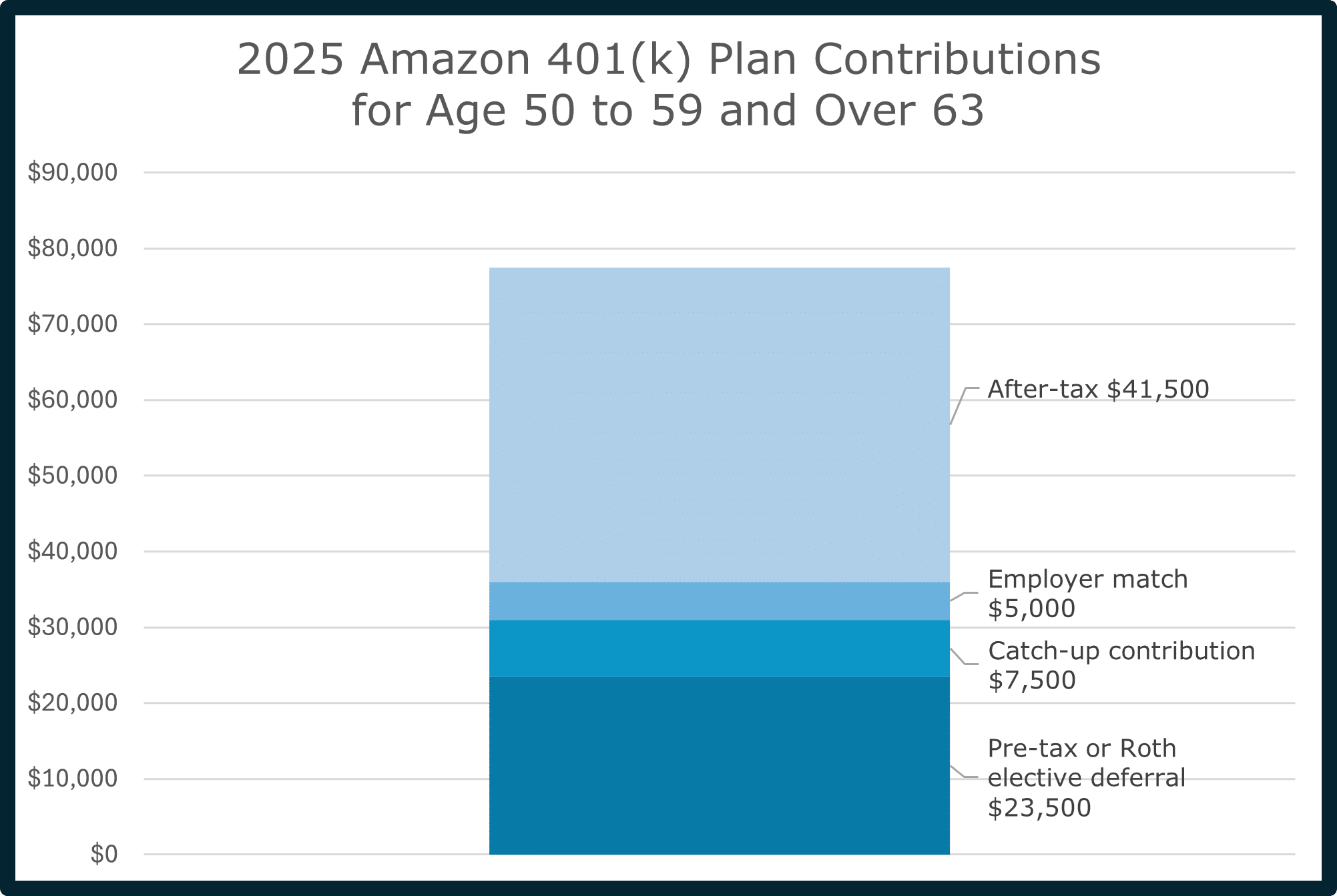

Age 50 to 59 and Over 63

- Elective deferral: $23,500

- Employer match: Up to $7,000*

- Catch-up contribution: $7,500

- After-tax contribution: ~$40,000**

- Total limit: $77,500

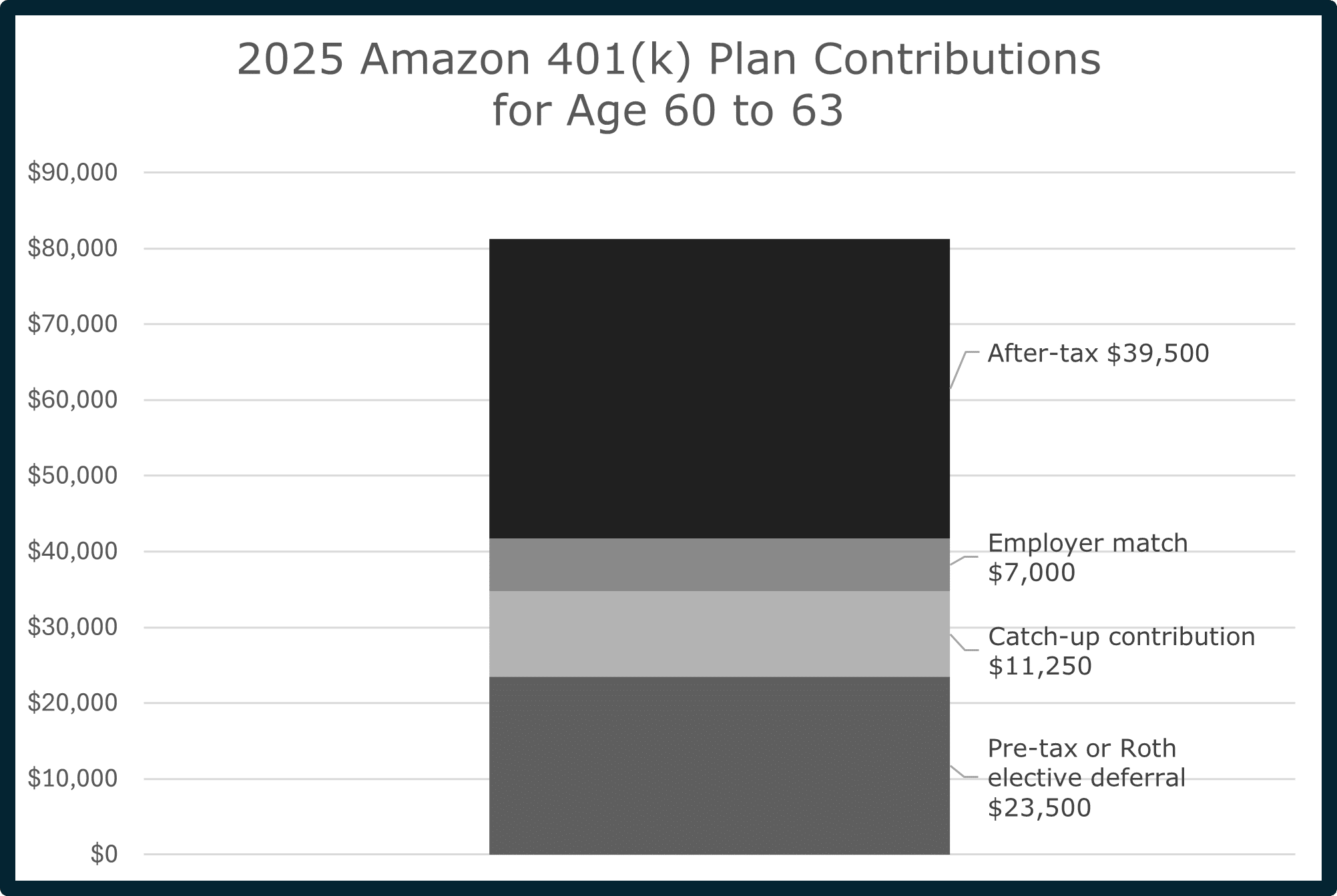

Age 60 to 63

- Elective deferral: $23,500

- Employer match: Up to $7,000*

- Catch-up contribution: $11,250

- After-tax contribution: ~$40,000**

- Total limit: $81,250

*Amazon matches 50% of elective deferrals up to 4% of eligible pay, with a maximum of $7,000. Catch-up contributions are not eligible for matching.

**For Amazon employees utilizing the mega-backdoor Roth strategy in 2025, the amount they can contribute as after-tax contributions is the difference between the total 401(k) contribution limit and the combined limits for elective deferrals, employer matching, and catch-up contributions.

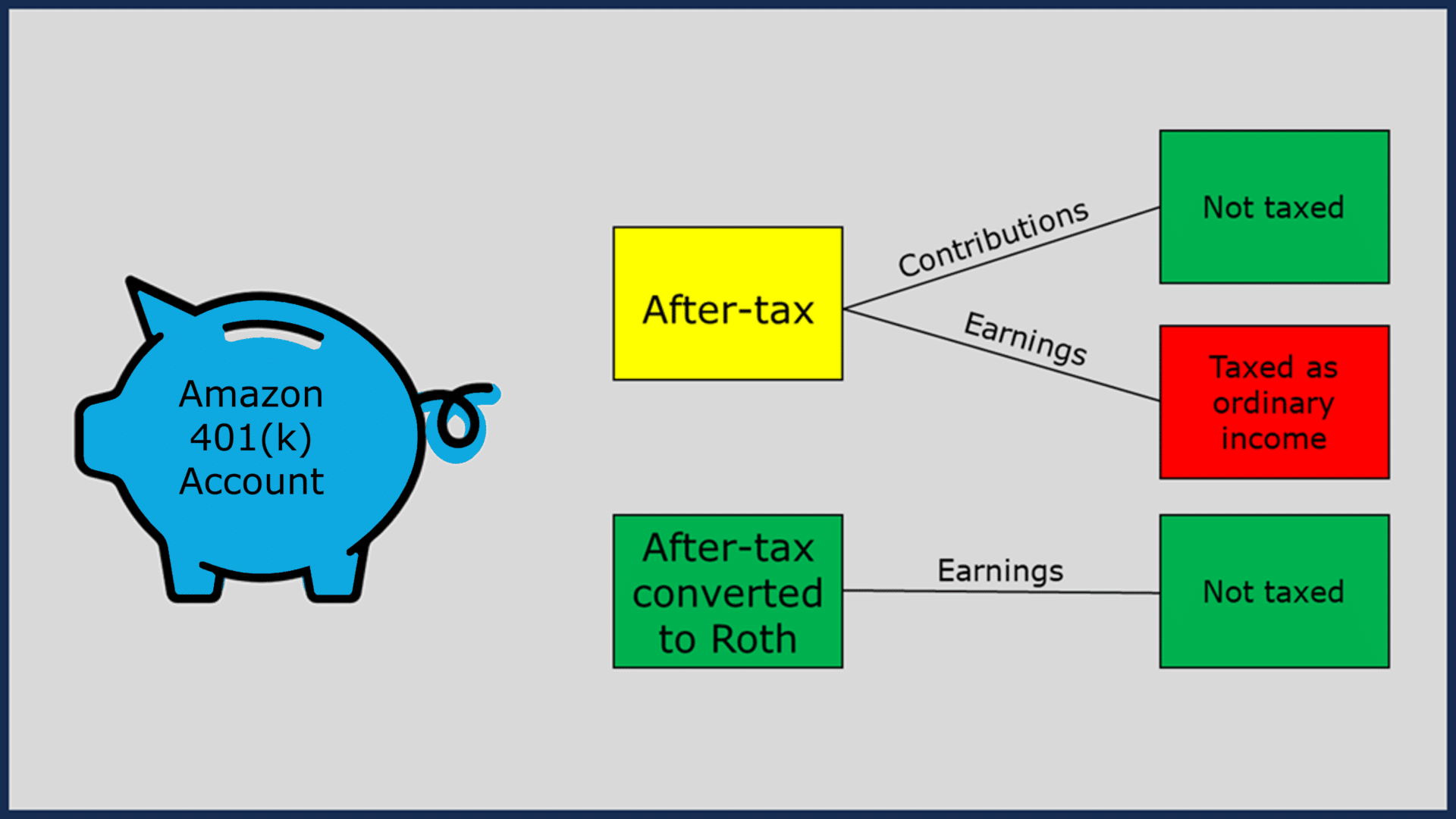

Amazon 401(k) Mega-Backdoor Roth Tax Consequences

After-tax 401(k) contributions are not taxed when distributed. However, if left untreated, after-tax earnings are taxed as ordinary income when distributed from the 401(k).

So, why would anyone utilize after-tax contributions? After-tax 401(k) contributions grow tax-free after the funds are converted to a Roth IRA or Roth 401(k). Without a Roth conversion, there are generally more tax-efficient ways to save for retirement than by participating in an after-tax 401(k).

How to Complete the Amazon Mega-Backdoor Roth Step-by-Step

Here are steps for executing the mega-backdoor Roth:

- Determine if the mega-backdoor Roth makes sense within your financial plan.

- Determine what percentage of your paycheck you want to allocate toward after-tax 401(k) contributions.

- Update the after-tax percentage online via Fidelity Net Benefits. Processing may take up to one or two pay cycles.

- Have a process in place for converting funds from after-tax 401(k) to Roth IRA or Roth 401(k).

Amazon Mega-Backdoor Roth Case Studies

Jeff – 60 years old

Jeff is a product manager at Amazon. Jeff earns $500,000 annually and wants to save more for retirement using the mega-backdoor Roth strategy.

- Jeff contributes $23,500 as an elective deferral and an additional $11,250 as a catch-up contribution.*

- Amazon matches $7,000.

- Jeff can contribute an additional $39,500 in after-tax savings.

*Important Note: The age 60 to 63 catch-up contribution is a new rule for 2025. Please confirm the amount with your 401(k) plan administrator.

Mark – 55 years old

Mark is an account executive at Amazon. Mark earns $250,000 annually and wants to save more for retirement using the mega-backdoor Roth strategy.

- Mark contributes $23,500 as an elective deferral and $7,500 as a catch-up contribution.

- Amazon matches $5,000.

- Mark can contribute an additional $41,500 in after-tax savings.

Kelly – 48 years old

Kelly is a senior director at Amazon. Kelly earns $300,000 annually and wants to save more for retirement using the mega-backdoor Roth strategy.

- Kelly contributes $23,500 as an elective deferral.

- Amazon matches $6,000.

- Kelly can contribute an additional $39,000 in after-tax savings.

Why the Amazon Mega-Backdoor Roth Matters in 2025

Most companies do not offer the mega-backdoor Roth strategy. Without a doubt, the mega-backdoor Roth is one of the most valuable benefits for high-income Amazon employees. The mega-backdoor Roth provides a lucrative opportunity for Amazon employees seeking to enhance tax-free retirement savings. However, it’s important to acknowledge that it’s not for everybody!

Here are some pros and cons for using the Amazon mega-backdoor Roth:

Pros

- The mega-backdoor Roth creates a tax-free savings opportunity.

- Investments grow tax-deferred.

- Funds can later be distributed tax-free during retirement.

Cons

- The mega-backdoor Roth is for long-term savings that are not easily accessible until retirement. Should you need funds sooner, then other account types may offer better accessibility.

- Pre-tax and Roth 401(k) contributions receive an employer match, but after-tax savings do not.

- Missing a step while attempting to complete this advanced planning strategy may unknowingly create a major tax headache for future you.

Take the time to determine if the mega-backdoor Roth is right for your unique financial situation. Consulting with a fiduciary financial planner can help provide peace of mind for you and your family.

If you’re an Amazon employee and have questions about after-tax 401(k) savings or the mega-backdoor Roth strategy, feel free to contact me at [email protected].

Amazon Mega-Backdoor Roth FAQs

1. Can I contribute to a traditional or Roth IRA in addition to the Amazon mega-backdoor Roth?

Yes. You can contribute to a traditional or Roth IRA in addition to the Amazon 401(k) and mega-backdoor Roth, as long as you stay within IRS limits.

If your income is too high to contribute directly to a Roth IRA, then you can use the backdoor Roth strategy alongside the mega-backdoor Roth to maximize your tax-free retirement savings.

2. What’s the backdoor Roth, and can I do both the backdoor Roth and mega-backdoor Roth as an Amazon employee?

The backdoor Roth IRA is a strategy for high-income earners who exceed the IRS income limits for direct Roth IRA contributions. It involves making a non-deductible contribution to a traditional IRA and then converting those funds to a Roth IRA.

In 2025, the IRA contribution limit is $7,000 for individuals under age 50 and $8,000 for those age 50 or older.

Yes, Amazon employees can use both strategies. The backdoor Roth is done through your personal IRA, while the mega-backdoor Roth is done through your Amazon 401(k) using after-tax contributions.

Combining both allows you to maximize tax-free retirement savings beyond standard limits.

Learn more about the backdoor Roth IRA strategy

3. What is the maximum Amazon mega-backdoor Roth contribution for 2025?

The total Amazon 401(k) contribution limit in 2025 depends on your age:

- $70,000 for employees under age 50

- $77,500 for employees age 50 to 59 and over 63

- $81,250 for employees age 60 to 63

4. Does Amazon match my after-tax 401(k) contributions?

No. Amazon only matches your pre-tax or Roth 401(k) elective deferrals—50% of the first 4% of eligible pay, up to $7,000 in 2025. After-tax contributions are not eligible for matching.

5. How often should I convert my Amazon after-tax 401(k) contributions to Roth?

To minimize taxable earnings, it’s best to convert after-tax contributions frequently, ideally after every paycheck or on a monthly schedule.

- If converting to Roth 401(k): Use Amazon’s automatic in-plan Roth conversion feature through Fidelity NetBenefits.

- If converting to a Roth IRA: You must manually initiate the conversion each time after the after-tax contribution posts.

6. How are earnings taxed for Amazon after-tax 401(k) contributions if I don’t convert?

If you don’t convert after-tax contributions to a Roth account, any earnings will grow and be taxed as ordinary income when withdrawn. Converting promptly allows those earnings to grow tax-free in a Roth account.

7. Can I withdraw money from my Amazon mega-backdoor Roth anytime?

While converted Roth contributions can typically be withdrawn tax-free, earnings must remain invested for at least five years and until age 59.5 to avoid taxes and penalties. This strategy is best used for long-term retirement savings.

8. If I leave Amazon, can I still make mega-backdoor Roth contributions?

No. You can’t make new after-tax contributions to Amazon’s 401(k) plan after leaving the company. However, you may be able to continue the strategy at a new employer if their 401(k) plan supports it.

9. Is the mega-backdoor Roth strategy worth it for high earners at Amazon?

Yes. For Amazon employees who max out their pre-tax or Roth 401(k) and want to save more for retirement, the mega-backdoor Roth is one of the most powerful strategies available. It allows for substantial tax-free growth that is otherwise unavailable to high-income earners.

10. What are the risks of the mega-backdoor Roth strategy?

- Missing the conversion step may result in taxable earnings.

- After-tax contributions are not matched by Amazon.

- Retirement funds are not easily accessible before retirement.

- The process for setting up the mega-backdoor Roth can be confusing and there are time-sensitive components to the conversion.

Working with a fiduciary financial planner can help ensure the strategy is executed correctly.

More Resources

Can I Make a Mega-Backdoor Roth Contribution? (Free PDF)

What Issues Should I Consider With My Employer-Provided Benefits? (Free PDF)

Mega-Backdoor Roth Guide

Financial Planning for Technology Professionals

Backdoor Roth Guide

Deferred Compensation Guide + Case Study

HSA Guide + Strategy for Reimbursement

RSU Guide + Strategy After Vesting

Disclosure: Safe Landing Financial is not affiliated, associated, or endorsed by Amazon. This information is supplied from sources that we believe to be reliable, however, we cannot guarantee the accuracy. All information is subject to change without notice.

Safe Landing Financial Newsletter

Sign up for monthly planning insights for tech professionals and pre-retirees!