RSU Guide: Tax and Vesting for Tech Professionals (2026)

Restricted stock units (RSUs) are one of the most valuable and most misunderstood forms of compensation for high-income tech professionals. For software engineers, product managers, and other tech employees at companies like Amazon, Dell, Google, and Meta, RSUs often represent a significant portion of total compensation, making the tax strategy around vesting one of the most important financial decisions you will make each year.

So if you want answers to questions like…

- What are key terms for RSUs?

- What are the tax consequences for RSUs?

- What should I do with RSUs after vesting?

… then this guide is for you!

Key terms for restricted stock units

Instead of giving away shares of stock, a company promises to give an employee a portion of stock gradually over a period of time.

RSUs are used to help incentivize employees to stay with and grow with a company long-term.

Depending on the performance of the company, RSUs can fluctuate in value.

Some important terms for RSUs are the grant date, vesting schedule, and vesting date.

RSU Grant

An RSU grant is a promise your company makes to give a number of shares in the future based on a vesting schedule.

RSU Vesting

RSU vesting is when you officially become the owner of the granted shares of stock.

RSU Grant Date

The grant date is the day your company promises to give a number of shares in the future based on a vesting schedule.

RSU Vesting Schedule

The vesting schedule is usually time-based and can also include performance metrics. Vesting schedules are usually graded, meaning a percentage of granted shares vest on specific days.

RSU Vesting Date

The vesting date is the day that you officially become the owner of the granted shares of stock.

Some events may cause granted shares to not reach the vesting date. Leaving a job early almost always stops vesting. When offering RSUs, a company shares a policy for how they treat RSU grants for retirement, disability, and death.

RSU Dividend and Voting Rights

RSUs don’t receive dividend or voting rights until the shares vest.

How are restricted stock units taxed?

RSUs have two tax triggers. Vesting causes ordinary income tax. Selling shares causes capital gains tax.

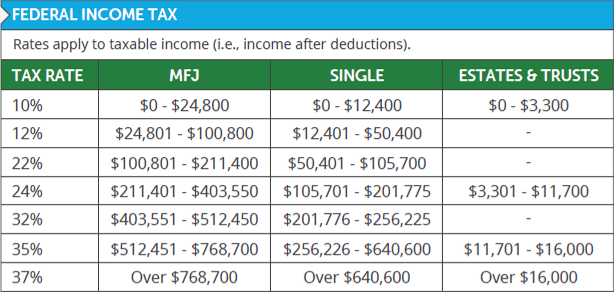

Vesting RSUs = Ordinary Income Tax

When shares vest, you’ll owe taxes for:

- Federal

- Social Security

- Medicare

- State

- Local

Many companies automatically sell 22% of RSUs at vesting to provide automatic tax withholding or may offer the option to adjust withholding.

Source: 2026 Important Planning Numbers

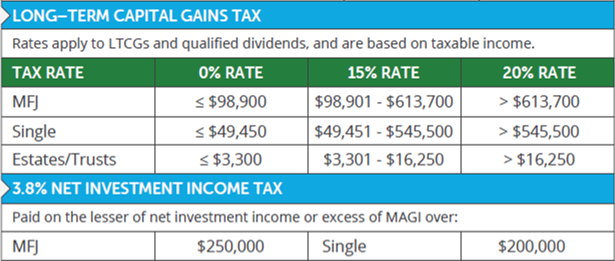

Selling RSUs = Capital Gains Tax

If your company enjoys high growth between the grant and vesting date, RSUs may cause a higher-than-expected tax bill.

If you sell shares right at vesting, then there are no taxable consequences for capital gains.

Selling after vesting causes taxable consequences for recognizing capital gains.

If held for under one year, selling vested RSUs causes a short-term capital gain which is taxed at your highest marginal tax rate.

If held for over one year, selling vested RSUs causes a long-term capital gain, which is generally taxed at 15% or 20% based on your income level.

If you’re receiving RSUs, then it’s important to be aware of the net investment income tax (NIIT) when selling RSUs. NIIT is an additional 3.8% tax for capital gains on modified adjusted gross income above $250,000 for married filing jointly or $200,000 for individuals.

Source: 2026 Important Planning Numbers

Should I sell or keep RSUs after vesting?

Your RSUs have vested… now what? Should you sell or hold the stock?

It depends.

How do the RSUs play into your long-term financial plan?

Consider the impact of a concentrated stock position within your portfolio.

Generally, I recommend having at least 95% of your total investments in a globally diversified portfolio based on your unique financial situation.

For those that enjoy picking investments outside of the strategic globally diversified portfolio, I have no problem with choosing 5% of one’s total investments. I call this portion of a overall portfolio as a “play account.”

I don’t recommend trading individual stocks if you don’t have the time, interest, discipline, and expertise for researching and managing a portfolio.

If you want to manage investments for the play account, would you rather hold your RSUs OR pick other investments such as stocks or cryptocurrency?

This is why, unless you have a strong opinion towards keeping the stock, it makes sense to sell RSUs at vesting. Remember, RSUs are just another form of income.

Why put your hard-earned dollars in one company?

What happens to your financial situation if your company goes bankrupt? Do you want one company controlling your income, benefits, 401(k) contributions and company match, and investments?

There are no additional incentives to keep the RSUs past vesting unless you believe the company is going to outperform the rest of the stock market. A diversified portfolio is much safer for planning your financial future.

Interested in working together?

Learn more about our complimentary 4-step process sharing how to minimize taxes, invest smarter, and make work optional. This process is designed to help decide if working together makes sense.

Restricted Stock Unit FAQs

1. What are restricted stock units (RSUs)?

Restricted stock units are a form of equity compensation where your employer promises to give you a specific number of company shares on a future date, based on a vesting schedule.

2. How are RSUs taxed at vesting?

When RSUs vest, the full market value of the shares is treated as ordinary income and taxed at your federal, state, and local income tax rates, as well as Social Security and Medicare. Most companies automatically withhold 22% for federal taxes at vesting, which is often not enough for high-income tech professionals in higher tax brackets.

3. Do I have to pay taxes on RSUs before I sell them?

Yes. RSUs are taxed as ordinary income at vesting regardless of whether you sell the shares. This is one of the most important areas to understand about RSUs. You owe taxes the moment the shares vest, even if you choose to hold them.

4. Should I sell RSUs immediately after vesting?

For most tech professionals, selling RSUs immediately at vesting is a solid choice. Since you already paid income tax on the shares at vesting, holding them adds concentrated stock risk on top of income already taxed. Unless you have a strong conviction that your company will outperform the broader market, a diversified portfolio is generally a safer long-term strategy.

5. What happens to my RSUs if I leave my company?

Unvested RSUs are typically forfeited when you leave your employer. Vested RSUs that have already been distributed as shares are yours to keep. Some companies offer accelerated vesting in cases of acquisition, disability, or retirement, so it is worth reviewing your RSU grant agreement carefully before making any job change decisions.

6. What is a concentrated stock position and why does it matter?

A concentrated stock position occurs when a single stock makes up a large percentage of your total investment portfolio. For tech professionals receiving RSUs, this often happens gradually without being noticed. Concentration in one company means your income, benefits, retirement contributions, and investments are all tied to the same employer, which significantly increases financial risk.

7. How do RSUs affect my tax bracket?

RSU income is added to your other income for the year and taxed as ordinary income. For high-income tech professionals, a large RSU vesting event can push you into a higher federal tax bracket, trigger the net investment income tax, or affect eligibility for certain deductions. Planning around your vesting schedule with a financial planner can help minimize the tax impact.

8. Do I need a financial advisor to manage my RSUs?

You are not required to work with a financial advisor, but RSU tax planning involves several moving parts including vesting timing, withholding rates, capital gains strategy, and portfolio concentration. A fee-only fiduciary financial planner who specializes in tech professionals can help you build a strategy that minimizes taxes and integrates your RSUs into a broader work-optional financial plan.

9. Is 22% withholding enough for RSUs?

For many high-income tech professionals, 22% withholding is not enough. The IRS default withholding rate for supplemental income is 22%, but if your total income puts you in the 24%, 32%, 35%, or 37% federal tax bracket, you will likely owe additional taxes at filing. A large RSU vesting event can create a significant unexpected tax bill if withholding is not adjusted proactively.

10. Can I withhold more than 22% on my RSUs?

Yes. There are several ways to increase the amount withheld or set aside for taxes on RSU income:

- Adjust withholding at your employer’s equity plan administrator: Some brokerage custodians allow you to request a higher withholding rate at vesting directly through their equity compensation platform. Check with your plan administrator to see if this option is available.

- Update your W-4: You can submit a new W-4 to your employer to increase federal income tax withholding from your regular paychecks to help cover the additional tax liability from RSU vesting.

- Make estimated tax payments: You can make quarterly estimated tax payments directly to the IRS to cover the gap between what is withheld and what you expect to owe.

Please note this is not tax advice. Everyone’s situation is different and the right approach depends on your total income, filing status, and other factors. Consult with a CPA or tax professional to determine the best strategy for your situation.

If you receive RSUs as part of your compensation and want help building a tax strategy around vesting, Safe Landing Financial offers fee-only financial planning for tech professionals. See if we’re a fit.

More Resources

Can I Make a Mega-Backdoor Roth Contribution? (Free PDF resource)

2026 Important Planning Numbers? (Free PDF resource)

Backdoor Roth Guide + Flowchart

RSU Guide + Strategy After Vesting

Deferred Compensation Guide + Case Study

HSA Guide + Strategy for Reimbursement

Investopedia Roth 401(k) vs. Roth IRA: What’s the Difference?

Business Insider Backdoor Roth IRA: Understanding the loophole that gives high-income earners the tax benefits of a Roth IRA

More Resources

What Issues Should I Consider Regarding My Restricted Stock Units? (Free PDF resource)

2026 Important Planning Numbers? (Free PDF resource)

Mega-Backdoor Roth Guide

Backdoor Roth Guide

Deferred Compensation Guide + Case Study

HSA Guide + Strategy for Reimbursement

Guide for RSUs at Dell

Forbes 5 Big Mistakes To Avoid With Stock Options And Restricted Stock Units

Safe Landing Financial Newsletter

Sign up for monthly planning insights for tech professionals and pre-retirees!