What to Do With a 401(k) After Leaving Your Job: Rollover Options Explained

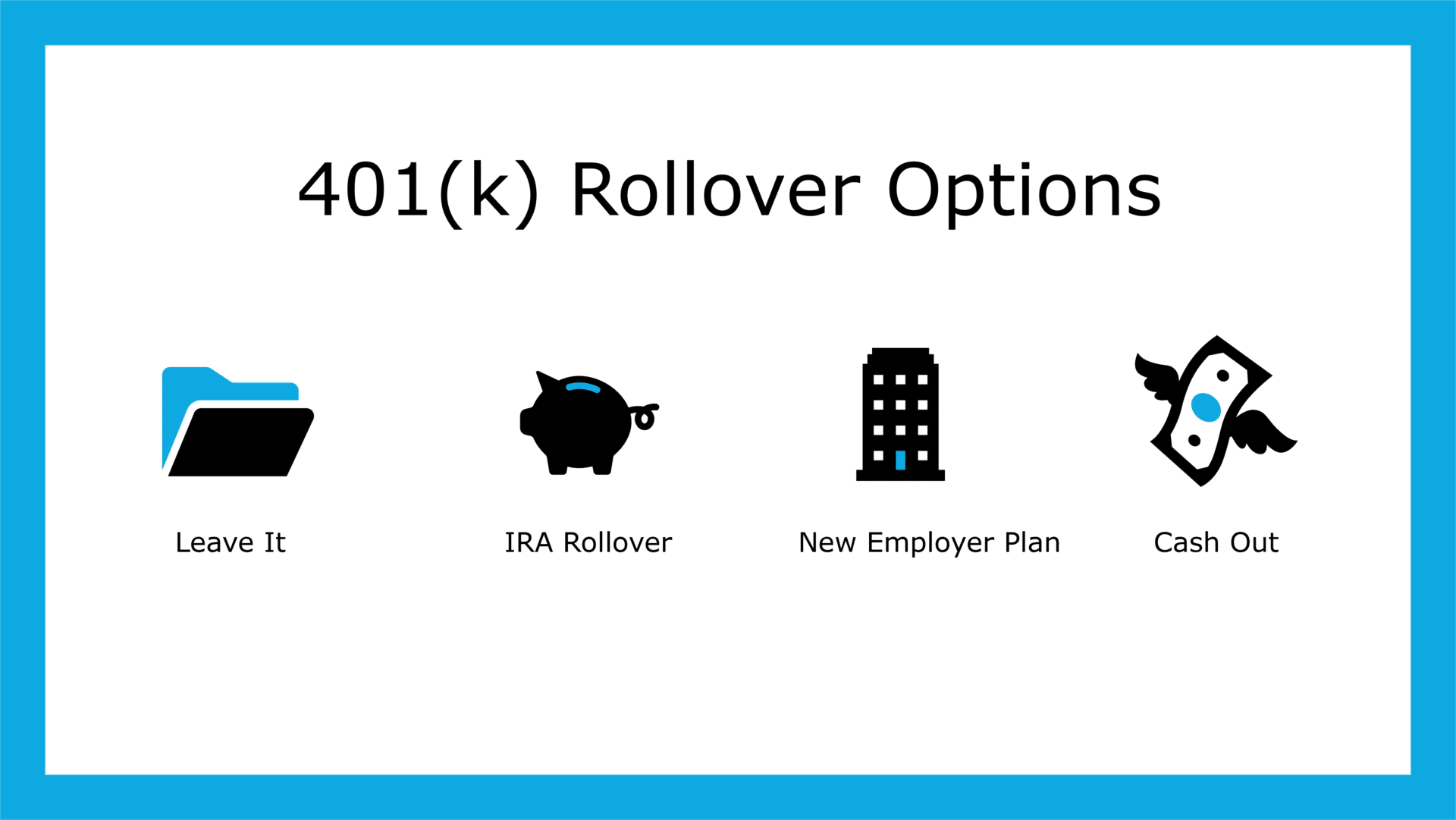

When you leave an employer, you may have an old 401(k) sitting that you’re unsure how to handle. Deciding what to do with an old 401(k) is an important step in keeping your financial plan on track. You generally have four choices: leave it where it is, roll it into your new employer’s 401(k), move it into an IRA, or cash it out. Each 401(k) rollover option comes with advantages and drawbacks, and the best choice depends on your overall financial goals.

1. Keep your money in your old 401(k)

Pros:

- Assets remain tax-deferred

- Strong creditor protection

- Penalty-free withdrawals as early as age 55 if you leave your employer

- Ability to delay required minimum distributions (RMDs) until after you leave work, if you are still employed

Cons:

- Investment options may be limited

- Plans often carry high fees with little transparency

- Harder to manage multiple accounts in your financial plan

2. Roll into your new employer’s 401(k)

Pros:

- Assets remain tax-deferred

- Creditor protection continues

- Penalty-free withdrawals at age 55 if separated from service

- Potential to borrow up to $50,000 from your account if the plan allows loans

- Easier tracking by consolidating accounts

Cons:

- Limited investment choices

- High or unclear fees are common

3. 401(k) Rollover to IRA

Pros:

- Assets remain tax-deferred

- Wide range of investment choices

- Transparent fee structures

- Typically lower costs compared to a 401(k)

Cons:

- Less creditor protection than a 401(k)

- No ability to borrow against the account

- Withdrawals generally restricted until age 59.5 without penalty

- RMDs must begin at age 73 (if you turn 72 after 2022) or age 75 starting in 2033.

4. Cash out your 401(k)

Pros:

- Immediate access to funds

Cons:

- Ordinary income taxes due right away

- Possible 10% early withdrawal penalty if under 59.5

- Sacrifices long-term tax-deferred growth

- Can push you into a higher tax bracket

Choosing the Best Path Forward

Your decision depends on your overall financial situation and retirement goals. For many people, rolling an old 401(k) into an IRA provides the most flexibility, transparency, and lower fees. Still, the right answer depends on your circumstances. Before making a move, consider consulting a fiduciary financial advisor who can help you weigh the tradeoffs and make a choice that fits into your broader plan.

More Resources

Financial Planning for Approaching Retirement

The Rule of 55: A Guide to Penalty-Free Early Retirement Income

Retirement Planning Roadmap Guide

Social Security Optimization Guide

Smart Tax Planning Guide

Retirement Planning Case Study

Work Optional Case Study

Nerdwallet: How to Find an Old 401(k) — and What to Do With It

Mega-Backdoor Roth Guide

Backdoor Roth Guide

Deferred Compensation Guide + Case Study

HSA Guide + Strategy for Reimbursement

RSU Guide + Strategy After Vesting

Safe Landing Financial Newsletter

Sign up for monthly planning insights for tech professionals and pre-retirees!